On May 10, 2025, the Sub-forum “Information Technology (IT) Transformation and High-quality Development of Financial Markets” of the 6th China Applied Economics Annual Conference (2025) (the “Sub-forum”) was successfully held in the Lingang VIP Hall of Shanghai Lingang Performing Arts Center.

Hosted by Dishui Lake Advanced Finance Institute, Shanghai University of Finance and Economics (SUFE-DAFI), the Sub-forum focused on the profound impact of IT innovation on financial markets. Scholars from top universities and research institutions across the country gathered to conduct in-depth discussions on the intersection of cutting-edge technologies (such as artificial intelligence, big data, and large language models) and financial markets.

The Sub-forum was co-hosted by Professor QIU Jiaping, Vice Dean of SUFE-DAFI, and TANG Yushan, Academic Director of the AI Finance Track and Associate Professor of SUFE-DAFI.

The Sub-forum was divided into two sessions, and eight high-level research results from key national universities were presented. These studies covered hot topics including expectation management of non-verbal information, large language models and market prediction, venture capital and public debt, crowdfunding platforms and innovative practices, and carbon credit subsidies, demonstrating diverse explorations and practical reflections on the in-depth integration of finance and IT.

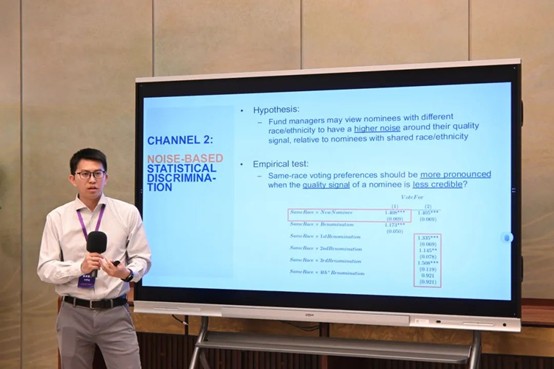

Professor YE Qiaozhi, Assistant Professor of SUFE-DAFI, introduced the collaborative paper Who do You Vote for? Same-race Preference in Director Elections. Using U.S. mutual fund voting data from 2005 to 2018, the research found that fund managers exhibited a significant “same-race preference” in director elections. This preference significantly increased the re-election probability of director candidates but had a limited impact on the performance of relevant funds, reflecting the hidden challenges faced by the diversity of corporate governance structures.

In her commentary, CAI Xini, Associate Professor of the International Business School at University of International Business and Economics (UIBE), affirmed the research’s novel perspective and solid data foundation. She also suggested further identifying the logical chain between preference mechanisms and corporate governance, enriching causal identification strategies, and conducting in-depth analysis of the heterogeneity in value orientations between funds and companies.

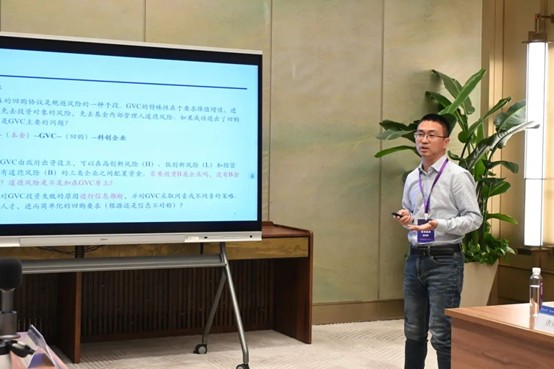

Professor ZHANG Yilin, Vice Dean of the Advanced Institute of Finance at Sun Yat-sen University, presented the paper The Formation and Evolution of GVC Repurchase Contracts: From the Two-tier Principal-agentPerspective.Based on the operation mechanism of government-backed venture capital (GVC), the research team proposed a “two-tier principal-agent model” to explain GVC’s preference for signing repurchase agreements. The research pointed out that repurchases in the early stage helped eliminate low-quality enterprises but may also inhibited high-risk innovation, thereby reducing overall social welfare. The authors further put forward a “targeted fault tolerance” policy suggestion, proposing to dynamically adjust the accountability mechanism according to GVC’s identification capabilities and development stages.

In his commentary, Professor XIONG Haifang, Vice Dean of the School of Finance at Northeast University of Finance and Economics, noted that the research addressed the institutional dilemma of “rigid repurchase redemption” and “lack of patient capital”. He suggested that future research should expand to topics such as the synergy mechanism between GVC and private venture capital (PVC), the impact of repurchase clauses on patent quality, and cross-border institutional applicability, providing practical references for China’s innovation governance.

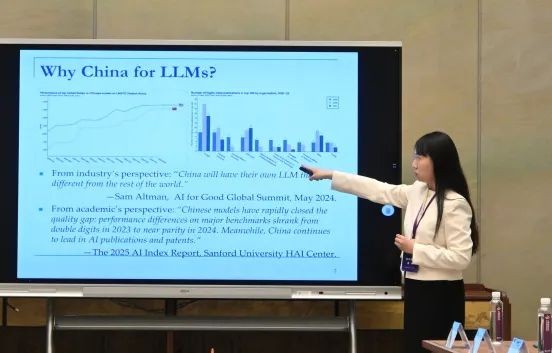

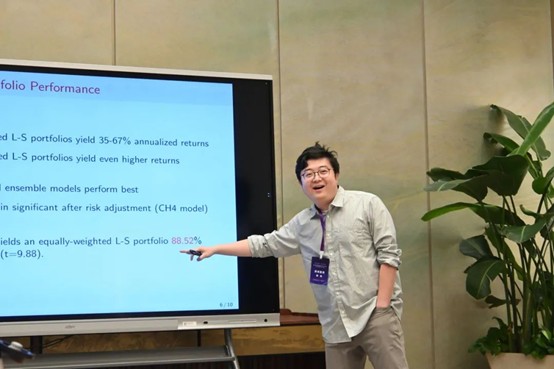

TAN Lin, Doctor of PBC School of Finance at Tsinghua University, shared the team’s latest research Large Language Models and Return Prediction in China. By using multiple large language models to process 28 million Chinese news articles, the research extracted text features to build a prediction model, achieving high-precision prediction of A-share returns. Empirical results showed that long-short portfolios built based on predictions could achieve significant annualized returns. Further analysis revealed that large model signals could predict earnings surprises prospectively, but investor responses exhibited significant heterogeneity.

In his commentary, ZHOU Hang, Associate Professor of the School of Finance at SUFE, suggested distinguishing the actual constraints of securities lending mechanisms on retail trading strategies, calling for further evaluation of AI’s impact on information fairness, and proposing to explore the integration path between AI and regulatory technology (RegTech).

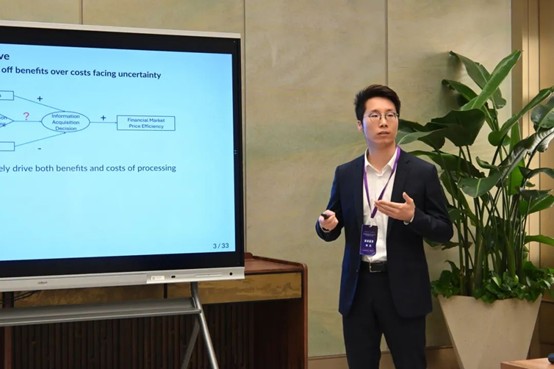

YANG Biao, Assistant Professor of the Antai College of Economics and Management at Shanghai Jiao Tong University, proposed the “sticky information cost hypothesis” in his paper Uncertainty and Market Efficiency: An Information Choice Perspective. He classified uncertainty into two types (“intrinsic” and “temporal”) and constructed an information cost indicator. Based on U.S. stock analyst forecast data from 1990 to 2019, the research found that expected errors in the high information cost group brought stronger tradable opportunities.

In his commentary, Professor ZHOU Kaiguo, Dean of the School of Finance at Capital University of Economics and Business, pointed out that the research provided a new explanatory path for information dissemination and market response mechanisms under high uncertainty. He suggested further expanding the theoretical applicability in combination with the characteristics of the Chinese market, such as extending the sample period, enhancing the expression of economic implications, and linking with policy guidance (e.g. supporting “specialized, refined, distinctive, and innovative” enterprises).

Professor DENG Xin, Assistant Dean of the Nanyang Business School at Nanyang Technological University, shared the paper From Pitch to Progress: The Interplay of Team Reputation and Governance in Crowdfunded Innovation. By comparing 4,014 ICO projects and 747 Kickstarter projects, the research pointed out that high-reputation teams were more likely to raise funds on platforms without governance constraints, but their innovation quality and the stability of raised funds tended to decline. In contrast, Kickstarter effectively prevented moral hazard and improved project delivery rates and long-term performance through institutional designs such as escrow, review, and milestone supervision, emphasizing the important constraint of institutional design on moral hazard.

In her commentary, Professor ZHANG Qunzi, Vice Dean of the School of Economics at Shandong University, noted that the research provided policy support for crowdfunding governance design. She suggested that regulatory authorities promoted the institutionalization and standardization of platform governance responsibilities to improve the robustness of the crowdfunding ecosystem.

FANG Minghao, Lecturer of the School of Finance at SUFE, introduced the collaborative research Venture Capital, Local Public Debt, and Corporate Innovation. By analyzing data from 25,000 A-share companies and 3,700 cities from 2006 to 2019, the research revealed the “debt-infrastructure-venture capital” synergy mechanism and put forward policy suggestions such as targeted support for sci-tech parks through special bonds and promotion of debt-venture capital linkage.

Professor MA Shuang, Vice Dean of the School of Economics and Statistics at Guangzhou University, believed that the research had a strong policy-oriented team. He suggested further strengthening the analysis of the bank credit control group and the characterization of patent quality indicators to enhance the explanatory power of results and policy applicability.

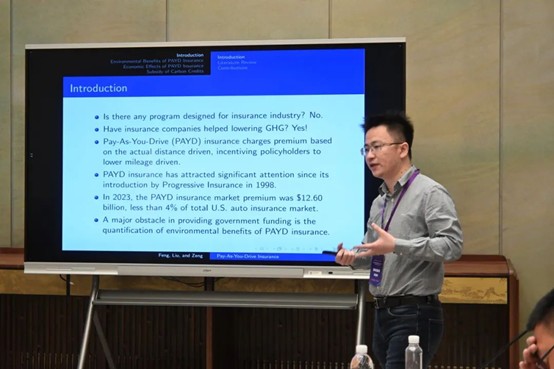

FENG Yulin, Associate Professor of the School of Finance at SUFE, reported on the paper Quantifying the Benefits of P-A-Y-D Insurance: Subsidy of Carbon Credit. By constructing a two-period dynamic model, the research measured the impact of Pay-As-You-Drive (PAYD) insurance on carbon emission reduction. It found that this mechanism could significantly reduce the annual mileage of vehicles, thereby increasing carbon credits per vehicle, but led to a decline in insurance company profits. The research proposed using carbon market revenues to subsidize insurers, promoting the implementation of green travel policies.

CAO Wei, Professor of the China Institute of Finance at Southwestern University of Finance and Economics, believed that the research’s model construction was rigorous. He suggested introducing more flexible utility functions to consider behavioral differences and fiscal sustainability assessments, enhancing the research’s practicality and policy implementation path.

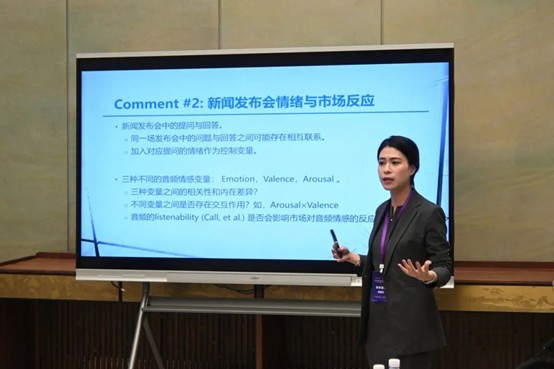

Professor LI Bin, Vice Dean of the School of Economics and Management at Wuhan University, shared the research The Expectation Management Effect of Non-verbal Information - From the Perspective of Multimodal Big Data. Based on a multimodal research of text and audio data from State Council Information Office press conferences (2013-2024), the research team pointed out that the audio emotion of speakers provided incremental information on market returns and volatility. When the audio emotion of speakers was more positive and intense, investor sentiment increased significantly and expected uncertainty decreases significantly, reflecting the “audio expectation management” mechanism in government communication.

XIAO Yuanyuan, Researcher of SUFE-DAFI, suggested strengthening the optimization of training sets for transfer learning and further revealing the interaction mechanism between audio signals and long-term market responses.

The rapid iteration of IT is profoundly reshaping the organizational model and operational logic of financial markets. The Sub-forum fully demonstrated the academic community’s keen insight and theoretical breakthroughs in the integration path of “technology + finance”, and also provided rich policy references for China in terms of institutional optimization, risk governance, and green development. In the future, the finance discipline should continue to deepen interdisciplinary collaboration and methodological innovation, promoting China’s financial system toward a higher level of resilience and high-quality development driven by technology.